.png)

By using our website, you agree to the use of cookies as described in our Cookie Policy

a

Rss Feed

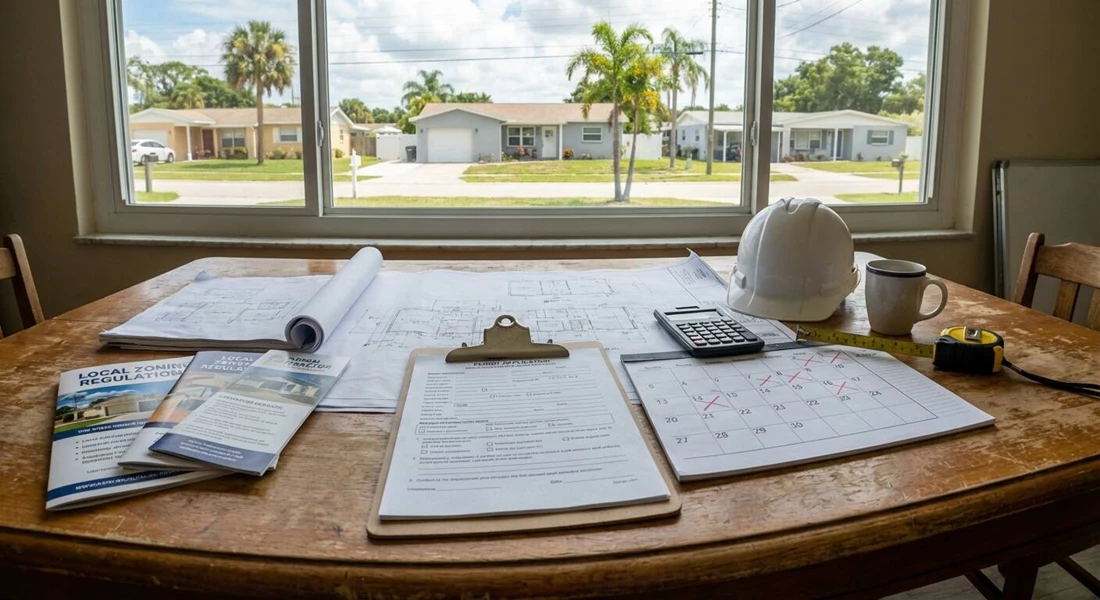

How Adding Onto Your Largo Home Can Affect Insurance

Add a new room or expand your house in Largo, and your insurance doesn’t automatically keep up. The extra space isn’t protected by your old policy. Insurers notice the bigger footprint and want to know what’s changing before you start. They’ll expect details up front. Otherwise, you’re not fully covered.

- Coverage limits set for your original home won’t stretch to cover new space.

- During construction, your risk profile changes. Fire, theft, and weather exposure all spike.

- Liability grows with every extra foot of living area. More space, more ways for accidents to happen.

- Replacement cost calculations shift. Your insurer needs updated numbers to keep you protected.

- Detached additions or new structures, like a pool house or workshop, often need their own riders.

Skip the insurance review, and you’re gambling with your investment. Work with our coastal home insurance specialists in Largo to lock in the right coverage before the first nail is driven. That’s how you avoid gaps that leave you exposed from day one.

Building Codes Shape Your Policy

Every addition in Largo faces a wall of building codes. Inspectors check hurricane straps, impact windows, and wind-resistant roofs. Insurance carriers do the same. Miss a single code requirement, and your policy can get voided or your premiums can jump overnight. They don’t care if your contractor “usually does it this way.” They want proof: permits, inspection reports, and contractor credentials. No paperwork, no payout.

When you plan a home addition in Largo’s coastal zone, expect your insurer to ask for:

- Permit copies for every phase of the project

- Inspection sign-offs for structural, electrical, and plumbing work

- Proof of code-compliant materials, especially for windows, doors, and roofing

- Contractor license and insurance documentation

Keep every document. Your insurance company will want to see it all. Lose the paperwork, and you lose leverage if a claim ever comes up. For renovation projects, the same rules apply. No shortcuts. No missing signatures. That’s how you keep your coverage solid and your premiums in check.

Flood Risk Changes With Every Addition

Flooding isn’t a distant threat in Largo. It’s a fact of life. Add a room, raise a deck, or build out a garage, and your flood risk changes instantly. Insurance companies know it. They’ll ask for new elevation certificates and updated drainage plans before they touch your policy. Skip these steps, and your rates can spike or your claim can get denied after the next big storm.

Designing an addition in a flood zone means:

- Getting a new elevation certificate for the expanded footprint

- Proving that drainage solutions meet current standards

- Documenting all flood-resistant construction details

Check the latest flood zone requirements before you start. Insurance rates in Largo can swing thousands of dollars a year based on a few inches of elevation or a missing drainage swale. Don’t let a simple oversight drain your budget or leave your new space unprotected.

Material Choices Hit Your Premiums

Insurance companies don’t just care about square footage. They care about what you build with. Pick the wrong materials, and your premiums climb. Choose the right ones, and you can lock in discounts that last for years. Impact-resistant windows, storm-rated doors, and reinforced roofing all work in your favor. Cheap siding, low-grade shingles, or non-compliant glass? That’s a fast track to higher costs and more exclusions.

When planning your addition, focus on:

- Impact-resistant materials for windows and doors

- Storm-rated roofing and fasteners

- Moisture-resistant flooring and wall systems

- Fire-resistant exterior finishes

Insurance carriers reward smart choices. See the full list of impact-resistant materials and storm-rated products that qualify for premium discounts. Don’t let a designer’s preference for looks cost you thousands in extra insurance every year. Build for strength, and your policy will reflect it. If you’re unsure which materials will help you save, we can walk you through the options that have proven to lower premiums for our clients in Largo.

What Happens If You Skip the Insurance Review

Plenty of homeowners finish their addition, then call their insurance agent. That’s backwards. Wait until after construction, and you risk:

- Denied claims for damage to the new space

- Gaps in liability coverage if someone gets hurt

- Outdated replacement cost numbers that leave you underinsured

- Premium hikes that could have been avoided with better materials or documentation

- Headaches with mortgage lenders who require proof of updated coverage

Insurance isn’t a box to check at the end. It’s a tool to protect your investment from the first day of construction. Get the right policy in place, and you’ll never have to wonder if your addition is covered when it matters most. If you’re planning a major addition, our team at Rose Building Contractors can coordinate with your insurance provider to help ensure your coverage is updated as your project progresses.

Ready to Build Smart in Largo?

Rose Building Contractors understands the delicate balance between beautiful design and insurance requirements. Call us at 727-596-2390 or contact us to discuss your addition plans today.

‹ Back

Recent Posts

-

How Long Does It Take to Build a Custom Home in Largo?

June 19, 2026

-

-

What Permits Are Needed for Home Additions in Largo?

June 5, 2026

-

-